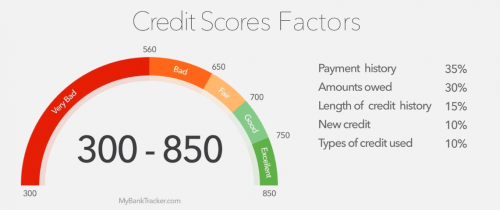

Bad credit history refers to a history of having difficulty paying your bills. This type credit history will reflect your financial behavior and show up in your credit report as a lower score. Low credit scores, usually below 580, make it more difficult to obtain a loan or credit card. These tips will help you improve your credit score.

On-time payment of your bills

You can improve your credit score by paying your bills on a timely basis. Avoid late fees and interest by paying only the minimum monthly payment. If you make late payments, your report could look different from one bureau. Keeping track of your payment history and disputing inaccurate information can help you improve your credit score. Remember that you cannot fix everything right away.

If you are having trouble paying your bills, you may be able to arrange a payment plan with them. They might offer an interest break, or you could choose a completely different payment schedule. You shouldn't make payments that are more than 4 months. It's better than having a higher debt/income ratio to pay off your accounts. You may be offered payment plans by credit card companies to meet your minimum monthly payments.

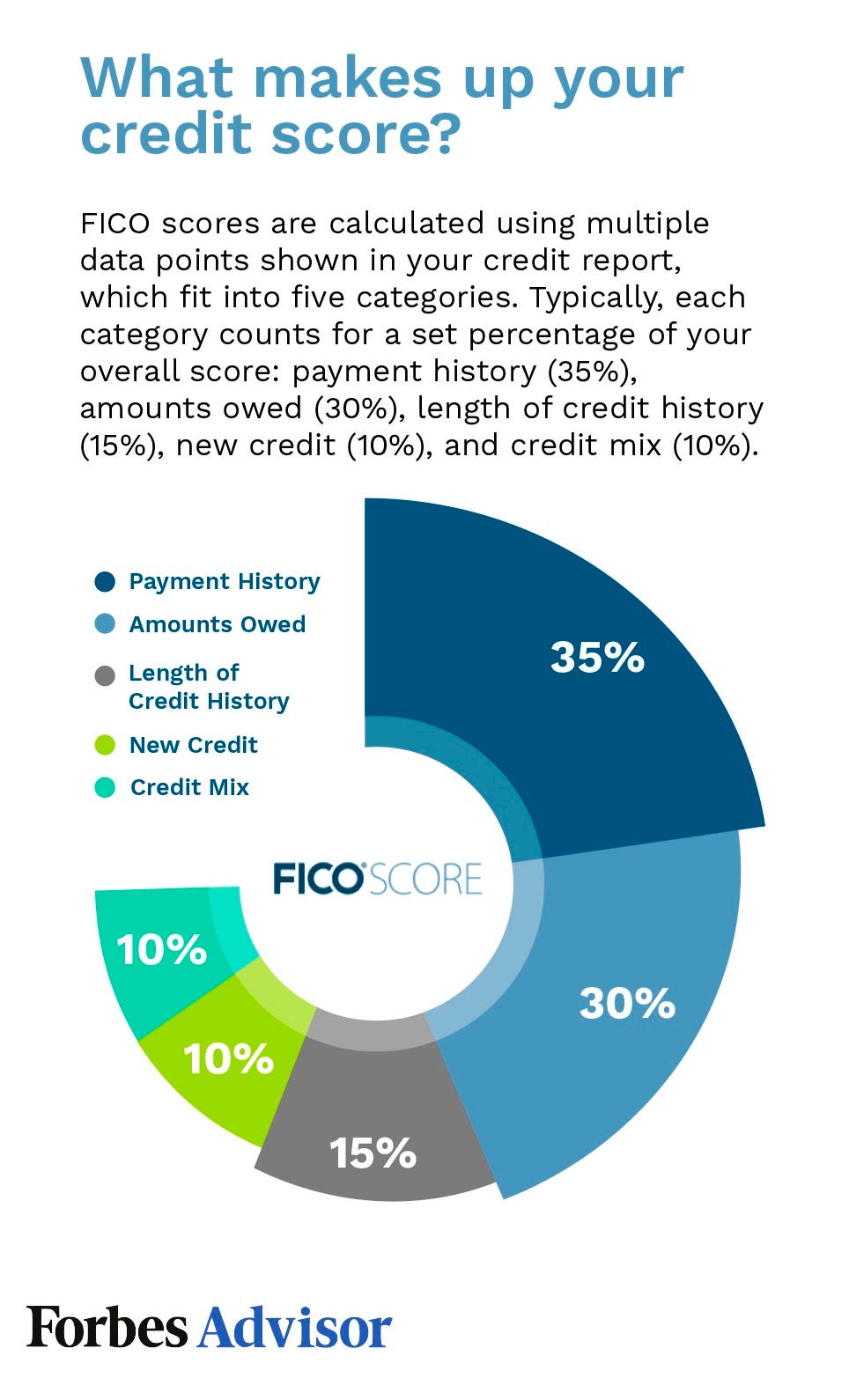

Payment history

Your payment history is very important. Your payment history is reported to the credit agencies by many creditors every month. This agency reports information about your payment history from many sources, including credit cards, retail accounts and installment loans. Public records such as judgments, foreclosures, wage attachments and judgments also include payment history. Paying on time and keeping a record of your past due balances can improve your credit score. On the other hand, late payments and missing payments can ruin your score.

Paying your bills on time is the best way to improve your credit score. Even though it's important to pay bills on time, sometimes life happens and our personal finances can take a back seat. One or two mistakes won't have any negative impact on our credit score. However, a long history is crucial. Creditors look at your payment history when determining if you are a good credit risk.

Credit history length

The length of credit history can have a significant impact on your credit score. The age of both your oldest and your newest credit accounts is taken into consideration when calculating your score. Your FICO score will increase the longer you have had credit history. Your credit history is more important than ever. The older your accounts, the more trustworthy you will be to creditors.

You must multiply your average credit age by the number years that you've had your credit accounts in order to calculate credit age. Eight years is the average age of credit cards. However, the length of individual accounts and the amount of time you've been using those accounts also play a role in determining your credit score. FICO does not publicly disclose these factors, so it is best to contact your lender to learn more about them.