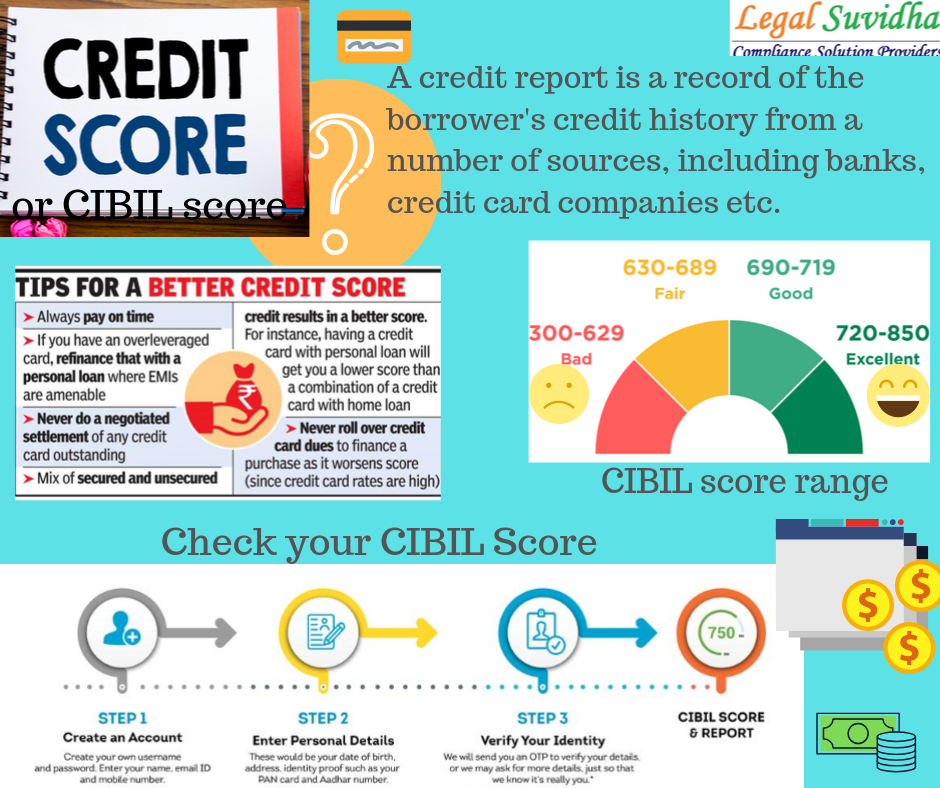

Credit rating tells you how likely it is that you will repay a debt. It implicitly predicts the likelihood that a debtor will default on payments. A credit rating is not only affected by the amount of time a person has been in debt for. Other factors also play a role. These include payment history and length of credit history as well as conflicts of interest.

Payment history

Your credit score will be based on your payment history. It is 35% responsible for your credit score. It informs lenders about your likelihood of paying your debts on time. While late payments won't affect your credit score, it can harm it. It is important to understand how your payment history impacts your credit score, and how you can improve it.

There is an easy and effective way to improve credit scores: Make your payments on schedule. This information is used by lenders and credit card companies to make lending decisions. Your payment history is the most important aspect of your overall credit history.

Credit history length

The length of credit history is an important factor in credit scores. It is responsible for 15% of your score. Other factors also play a role, but the better your credit history, and the more you will score, is. Lenders love long-term customers who are punctual with their payments.

Your credit report contains information about the length of credit history. It is used for determining your reliability. It is possible to improve your score by having an account for at minimum three years. Creditors will be more likely to lend you money if your credit history is long.

Credit mix

It shows lenders that you can responsibly manage your debt by having multiple credit accounts. Your credit profile is about 10% of the credit score. You should be aware that your credit mix may fluctuate from time to time. These fluctuations do not have any lasting impact on credit scores.

Good credit mixes include both revolving as well as installment credit. Revolving credit should be paid in minimum monthly installments. In installment credit, you shouldn't charge more than you can afford to pay each month. You also should avoid interest. Similarly, if you have a high credit limit and don't have any installment credit, consider taking out a small personal loan to demonstrate that you can manage different kinds of credit.

Conflicts of interests

Conflicts of interest in credit rating industry are not without their problems. Among them are the fact that most credit rating agencies receive compensation for their ratings. This leaves them open to conflicts of Interest. Additionally, agencies could have a conflict if they were involved with creating credit ratings. These issues have also led Congress to investigate the issue. There are steps companies can take in order to avoid conflicts.

Reviewing the regulations of SEC is the first step. The SEC has a number of regulations in place regarding the conflict of interest of rating agencies. These guidelines are applicable to both rating agency-owned and issuer-paid companies. These regulations prevent conflicts from affecting quality ratings assessments.

Agents charge fees

Numerous rating agencies charge issuers a fee for their services. These fees can be negotiable, and will depend on the bond size and type of security. An issuer should communicate with the rating agency in advance about how many ratings they need. It is crucial to understand the fee structure prior to signing rating documents. Credit rating companies must sign a contract and should not be tempted by an increase in the fee.

A credit rating agency's service to a borrower depends on its reliability. Low credit ratings can affect a borrower’s financial position. An independent credit rating agency must be credible and credible. A quality agency will provide objective ratings for companies and investors.